The global psychometric tests market is experiencing robust and sustained expansion, fueled by the intersection of digital HR transformation, evidence-based talent management, and artificial intelligence integration. Psychometric assessments have evolved from paper-based clinical instruments into sophisticated digital platforms that deliver real-time, predictive insights into cognitive ability, personality, behavioral tendencies, and emotional intelligence.

Key highlights from this report:

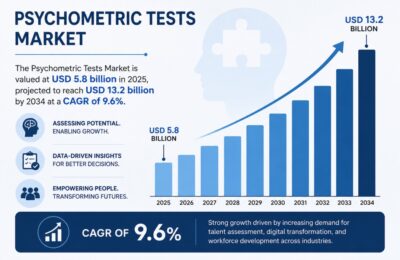

- Market valued at USD 5.8 billion in 2025, projected to reach USD 13.2 billion by 2034 at a CAGR of 9.6%.

- Online delivery accounts for 71.5% of total revenues in 2025, reflecting accelerated digital adoption.

- North America holds the dominant regional share at approximately 38.4% of global revenues.

- AI-adaptive testing platforms are reducing assessment time by 30–40% while improving measurement precision.

- The top ten vendors collectively hold 54–58% of global market revenues in 2025.

- Recruitment & Selection represents the largest application segment, accounting for 48% of market revenue.

- Skills-based hiring is projected to be the default paradigm for over 85% of Fortune 1000 companies by 2034.

2. Market Overview & Definition

Psychometric tests are scientifically designed assessments that measure psychological attributes including cognitive abilities, personality traits, aptitude, emotional intelligence, and behavioral tendencies. Unlike conventional interviews or basic knowledge quizzes, psychometric instruments are grounded in established psychological theory and validated empirically through large normative samples.

These assessments are deployed across a wide spectrum of use cases including pre-employment screening, leadership development, workforce planning, clinical diagnostics, educational placement, and employee wellness programs. The growing complexity of job roles, expanding global workforces, and the increasing emphasis on diversity and inclusion have collectively elevated psychometric testing from a supplementary HR tool to a mission-critical component of strategic talent management.

2.1 Historical Context

Psychometric assessment has its roots in the late 19th and early 20th centuries, with pioneers such as Francis Galton, Alfred Binet, and Charles Spearman laying the theoretical foundations of intelligence and personality measurement. The Stanford-Binet Intelligence Scale, developed in 1916, and the Myers-Briggs Type Indicator (MBTI), introduced in the 1940s, became widely adopted instruments in educational and occupational settings.

The commercialization of psychometric testing accelerated through the latter half of the 20th century, as organizations began standardizing their hiring processes in response to regulatory requirements around equal employment opportunity and the growing body of research demonstrating the predictive validity of structured assessments. The advent of the internet in the 1990s and early 2000s enabled the first wave of online test delivery, dramatically expanding accessibility and reducing administration costs.

2.2 Modern Market Landscape

Today, the psychometric tests market encompasses a diverse ecosystem of test publishers, technology platforms, consulting firms, and specialized niche providers. The industry has shifted from product-centric selling (individual test licenses) toward integrated platform models that combine assessment libraries, talent analytics dashboards, applicant tracking system (ATS) integrations, and AI-powered scoring engines.

3. Market Size & Forecast

The global psychometric tests market demonstrated consistent growth through the forecast period, underpinned by structural demand drivers in corporate HR, education, and clinical psychology. Market sizing across research sources varies based on scope definitions; this report synthesizes consensus estimates from multiple primary and secondary sources.

3.1 Global Market Size Summary

| Metric | 2023 | 2025 | 2034 |

| Market Size (USD) | — | $5.8 Billion | $13.2 Billion |

| CAGR (2026–2034) | — | — | 9.6% |

| Online Delivery Share | — | 71.5% | ~82% (est.) |

| North America Share | ~38% | 38.4% | ~38% |

| AI R&D Investment | — | $620M+ | ≈15%+ annual growth |

| Fortune 1000 Using Skills-Based Hiring | — | ~60% | >85% (projected) |

3.2 Growth Drivers

Several converging forces are accelerating market growth:

Rise of Skills-Based and Data-Driven Hiring

Organizations are moving away from credential-based hiring toward objective, competency-focused evaluation frameworks. Psychometric tests provide standardized, bias-mitigating data points that complement resume screening and interviews. Over 61% of U.S. organizations now use psychometric or cognitive evaluation platforms, and 48% have deployed AI-powered pre-employment testing.

AI and Adaptive Testing Technology

Artificial intelligence and machine learning are fundamentally transforming test design, delivery, and scoring. AI-powered adaptive testing platforms use Item Response Theory (IRT) algorithms combined with neural network models to dynamically adjust item difficulty, sequence, and format based on real-time test-taker responses. This results in shorter, more precise assessments that reduce test fatigue while increasing measurement accuracy. Global investments in AI-driven psychometric R&D exceeded USD 620 million in 2025, with annual growth rates above 15% expected through 2034.

Remote Work and Virtual Hiring

The normalization of remote and hybrid work arrangements has accelerated adoption of digital assessment platforms. Organizations now conduct assessment and hiring processes entirely online, driving demand for secure, proctored, and scalable psychometric delivery infrastructure.

Mental Health and Employee Wellness

Growing corporate awareness of mental health has expanded the scope of psychometric use beyond recruitment into clinical diagnostics, wellness screening, and therapeutic applications. Organizations are deploying personality and emotional intelligence assessments within employee assistance programs (EAPs) and leadership development curricula.

Diversity, Equity, and Inclusion (DEI) Initiatives

Structured psychometric assessments are increasingly adopted as tools for reducing unconscious bias in hiring and promotion. Scientifically validated tests offer a more equitable basis for candidate evaluation compared to unstructured interviews, which are particularly susceptible to affinity bias.

3.3 Market Restraints

- Limited awareness and understanding of psychometric tests among small and mid-market employers, particularly in emerging markets.

- Concerns around cultural bias and the risk that test norms developed in Western contexts may not translate equitably across global or diverse populations.

- Data privacy and security concerns, particularly under frameworks such as GDPR in Europe and CCPA in California, which impose strict requirements on the collection, storage, and use of psychometric data.

- Perceived complexity and high implementation costs associated with enterprise-grade psychometric platforms.

- Candidate skepticism about the validity and fairness of automated assessment decisions.

4. Market Segmentation

4.1 By Test Type

The psychometric tests market is segmented by assessment type, with each category serving distinct evaluation objectives across the talent and clinical spectrums.

| Test Type | 2024 Share | 2025 CAGR | Key Application |

| Aptitude / Ability Tests | ~36% | 9.8% | Corporate Recruitment |

| Personality Tests | ~24% | 9.3% | Leadership & Culture Fit |

| Cognitive Ability Tests | ~28% | 9.1% | Academic & Corporate Hiring |

| Behavioral Assessments | ~8% | 10.2% | Team Fit, Coaching |

| Emotional Intelligence Tests | ~4% | 11.0% | Leadership Development |

Aptitude and cognitive tests collectively dominate the market due to their high predictive validity in relation to job performance. Personality assessments, led by instruments such as the Hogan Personality Inventory (HPI) and the Big Five frameworks, are central to leadership selection and organizational culture alignment. Emotional intelligence assessments are the fastest-growing sub-segment, reflecting increased recognition of EQ as a performance predictor, particularly in management and customer-facing roles.

4.2 By Application

The application segmentation reflects the end-use context in which psychometric assessments are deployed:

| Application | Market Share | 2025 CAGR | Description |

| Recruitment & Selection | ~48% | 9.4% | Pre-employment screening & candidate ranking |

| Training & Development | ~27% | 10.4% | Competency mapping & learning pathways |

| Clinical & Counseling | ~14% | 8.8% | Diagnostics, therapy, wellness programs |

| Educational Assessment | ~7% | 8.5% | Academic placement & career guidance |

| Others (Gov., Military) | ~4% | 9.0% | Security clearances, public sector hiring |

4.3 By Delivery Mode

Online delivery has become the dominant channel, accounting for 71.5% of total market revenues in 2025. Cloud-based platforms offer significant advantages in scalability, accessibility, and integration with applicant tracking systems (ATS). Mobile-based assessment is an emerging sub-trend, driven by candidate expectations for seamless, device-agnostic test experiences. Offline and paper-based delivery retains relevance in clinical psychology, regulated environments, and regions with limited digital infrastructure.

4.4 By End-User

Corporate organizations represent the largest end-user segment, accounting for approximately 55% of market revenue. Educational institutions represent the second-largest segment, followed by government and public sector entities. Healthcare and clinical settings are a growing end-user category as mental health screening becomes integrated into preventive healthcare programs.

5. Regional Analysis

5.1 North America

North America dominates the global psychometric tests market, accounting for approximately 38.4% of total revenues at USD 2.23 billion in 2025. The region benefits from a mature HR technology ecosystem, high enterprise adoption rates, strong research infrastructure, and the presence of leading vendors including SHL, Criteria Corp, HireVue, and Korn Ferry. The United States alone accounts for approximately 21.4% of global revenues in the psychological testing software segment. Federal and state agencies conduct millions of psychometric assessments annually, reinforcing validation and demand infrastructure. North America is forecast to grow at a CAGR of 8.7% through 2034.

5.2 Europe

Europe is the second-largest regional market and is expected to record the fastest CAGR growth during the forecast period. The United Kingdom, Germany, France, Italy, and the Netherlands are the leading adopter countries. The UK has a particularly deep-rooted tradition of occupational psychometric assessment, with major global vendors SHL and Saville Assessment both headquartered in England. European organizations have incorporated psychometric testing extensively into structured hiring and professional development frameworks. The GDPR framework, while creating compliance complexity, has also encouraged vendors to invest in privacy-compliant, ethically grounded assessment practices that are gaining global acceptance.

5.3 Asia-Pacific

Asia-Pacific represents the fastest-growing emerging region, with several sources citing the region holding over 45% share by 2026 in specific segments, driven by the semiconductor, financial services, and technology hubs of China, India, Japan, South Korea, and Australia. The rapid growth of multinational corporations and domestic enterprises in these markets, combined with increasing adoption of Western HR practices, is generating substantial demand for standardized psychometric platforms. India is a particularly significant growth driver, with a large English-speaking professional workforce and a well-established domestic psychometric testing industry.

5.4 Latin America, Middle East & Africa

Latin America and the Middle East & Africa (MEA) represent nascent but high-potential markets. Brazil, Mexico, South Africa, the UAE, and Saudi Arabia are identified as priority growth geographies. Rising mental health awareness, expanding corporate sectors, and government investments in workforce development are creating favorable conditions for market entry. Localization of test instruments and culturally adaptive norms represent critical success factors in these regions.

6. Competitive Landscape

The psychometric tests market exhibits a moderately consolidated competitive structure at the premium enterprise end, with a fragmented long tail of specialist niche providers, regional vendors, and emerging technology-first challengers. The top ten vendors collectively account for an estimated 54–58% of total global market revenues in 2025, with the remaining share distributed among hundreds of smaller players.

6.1 Key Players Overview

| Company | Headquarters | Key Strengths |

| SHL | United Kingdom | Enterprise aptitude testing, OPQ32 personality, AI talent intelligence |

| Hogan Assessments | United States | Personality-based job performance prediction, leadership selection |

| Korn Ferry | United States | Integrated talent management, executive search & psychometric assessments |

| Aon Assessment Solutions | United Kingdom / Global | Pre-employment testing, AI-adaptive modules, workforce analytics |

| Pearson TalentLens | United States | Cognitive and aptitude testing, educational & clinical assessment |

| The Myers-Briggs Company | United States | MBTI personality assessment, team dynamics, leadership development |

| Criteria Corp | United States | SMB-focused online pre-employment testing, cognitive & personality |

| Thomas International | United Kingdom | Behavioral & cognitive assessments, DEI hiring tools |

| HireVue | United States | AI-powered video interviewing with integrated psychometric scoring |

| Mercer Mettl | India / Global | Online proctored assessments, emerging market focus |

6.2 Competitive Dynamics

Competitive differentiation in the psychometric tests market operates across several dimensions:

- Scientific rigor and validated evidence — vendors invest in peer-reviewed validation studies demonstrating predictive validity and construct reliability.

- Platform technology capabilities — AI-driven adaptive testing, real-time analytics dashboards, and seamless ATS integrations.

- Depth of HCM integration partnerships — alliances with Workday, SAP SuccessFactors, Oracle HCM, and Greenhouse are critical for enterprise sales.

- Breadth of assessment library — comprehensive catalogs spanning cognitive, personality, behavioral, and situational judgment tests.

- Localization and multilingual support — validated translations in 30+ languages for global deployment.

- Gamification and candidate experience — next-generation vendors are embedding game-based assessment mechanics to improve completion rates and reduce candidate anxiety.

6.3 Recent Market Developments

- SHL launched its AI-powered Talent Intelligence Suite in 2024, integrating psychometric data with workforce analytics and succession planning tools.

- Leading vendors including SHL, HireVue, and Aon Assessment Solutions launched AI-adaptive psychometric modules between 2024 and 2026 that reduce average testing time by 30–40%.

- Increasing M&A activity: private equity investment and strategic acquisitions are consolidating niche providers into broader talent technology platforms.

- Subscription-based and enterprise licensing pricing models are replacing per-test transaction models, improving revenue predictability.

- Launch of short-form adaptive assessments designed to reduce candidate fatigue and optimize screening time in high-volume hiring environments.

7. Emerging Trends & Technology

7.1 Artificial Intelligence & Machine Learning

AI and ML are the most transformative forces reshaping the psychometric testing landscape. Modern adaptive testing engines use Item Response Theory (IRT) combined with deep learning models to dynamically calibrate item selection in real time. This results in assessments that are simultaneously shorter, more precise, and more engaging for candidates. Predictive validity coefficients for AI-augmented tests are showing improvements of 15–25% over traditional fixed-form equivalents in controlled studies.

Natural language processing (NLP) is enabling new categories of open-ended response assessments, where candidates’ free-text answers are scored automatically against validated competency frameworks. Video-based assessments combining facial expression analysis, speech pattern recognition, and content scoring are an emerging frontier, though they raise significant fairness and bias considerations.

7.2 Gamified Assessments

Gamification represents one of the most significant innovations in candidate experience design. Game-based assessments embed psychometric measurement within engaging, interactive scenarios that reduce the artificiality of traditional testing contexts. Research indicates that gamified assessments improve candidate completion rates by 25–40% and deliver equivalent or superior predictive validity to conventional formats. Vendors such as Pymetrics (now part of Harver) and Arctic Shores have pioneered this category.

7.3 Neuroscience-Based Assessment

A frontier segment within psychometric testing applies neuroscientific principles to behavioral measurement, using cognitive tasks designed to activate specific neural pathways associated with executive function, working memory, and decision-making under uncertainty. These assessments are particularly relevant for high-stakes roles in financial services, defense, and senior executive selection.

7.4 Continuous and Longitudinal Assessment

Rather than treating psychometric assessment as a discrete pre-hire event, progressive organizations are adopting continuous measurement frameworks that track cognitive and behavioral indicators throughout the employee lifecycle. Integrated talent management platforms enable longitudinal benchmarking that supports performance management, career development, and succession planning.

7.5 Data Privacy and Ethical AI

As psychometric data becomes increasingly sensitive under global privacy regulations, vendors are investing in privacy-by-design architectures, differential privacy techniques, and third-party audit frameworks. The ethics of algorithmic decision-making in hiring is receiving growing regulatory scrutiny; the EU AI Act (in force from 2025) classifies AI systems used in employment screening as high-risk, imposing conformity assessment, transparency, and human oversight requirements.

8. Industry Verticals & Application Deep-Dive

8.1 Corporate Sector

The corporate sector is the primary demand engine for psychometric testing, accounting for approximately 55% of global market revenues. HR departments across industries deploy psychometric platforms at multiple stages of the talent lifecycle: pre-hire screening, onboarding assessments, learning and development profiling, high-potential identification, succession planning, and leadership development.

Industries with particularly high psychometric adoption rates include financial services, technology, consulting, pharmaceutical and life sciences, and manufacturing. In financial services, integrity and risk-tolerance assessments are deployed alongside cognitive ability tests to evaluate candidates for trading, advisory, and compliance roles. Technology companies rely heavily on cognitive and technical skill assessments integrated into automated applicant screening workflows.

8.2 Educational Sector

Educational institutions use psychometric assessments for student selection, learning disability identification, gifted program placement, career counseling, and academic performance prediction. Universities and business schools in the UK, Europe, and increasingly Asia-Pacific have integrated psychometric instruments into admissions and student support processes. The growth of competency-based education and personalized learning platforms is creating demand for adaptive psychometric tools that can continuously assess student progress and adapt curriculum delivery.

8.3 Clinical and Healthcare Sector

Clinical psychologists, psychiatrists, and healthcare providers use standardized psychometric instruments for diagnostic assessment, treatment planning, outcome monitoring, and forensic evaluation. Key instruments in this segment include the MMPI-3 (Minnesota Multiphasic Personality Inventory), Beck Depression Inventory, and various neuropsychological test batteries. The integration of psychometric screening into telehealth and digital mental health platforms represents a significant growth opportunity, as mental health awareness increases globally and access to in-person clinical services remains constrained.

8.4 Government and Public Sector

Government agencies and military organizations represent a significant institutional buyer segment, deploying psychometric assessments for civil service recruitment, security clearance evaluation, and military personnel selection. Government assessment mandates create predictable, large-scale demand for validated testing infrastructure. In the United States, federal agencies process millions of psychometric assessments annually through platforms such as USAJobs and OPM’s assessment center framework.

9. Porter’s Five Forces Analysis

Threat of New Entrants — Moderate

While the core technology infrastructure for online test delivery has become more accessible, the psychometric tests market retains significant barriers to entry including: the need for extensive normative validation research; IP protection around established test instruments; deep integration partnerships with enterprise HR platforms; and brand trust built over decades of deployment. Emerging AI-native startups are entering the market with innovative formats but face challenges in achieving the scientific credibility and enterprise trust required for large-scale adoption.

Bargaining Power of Buyers — Moderate to High

Enterprise buyers, particularly large multinational corporations and government agencies, hold significant negotiating leverage due to their scale. The proliferation of assessment vendors and increasing commoditization of basic cognitive testing are giving buyers more alternatives and driving price compression in standard assessment categories. However, for specialist and validated instruments with established track records, buyer power is moderated by switching costs and the risk of disrupting validated hiring processes.

Bargaining Power of Suppliers — Low to Moderate

The primary inputs to psychometric test development are intellectual capital (psychometricians, I/O psychologists), cloud infrastructure, and technology platforms. Cloud infrastructure is a commodity; psychometric expertise is specialized but not scarce enough to create significant supplier power. Key talent in AI and psychometric science is in demand across industries, creating moderate labor market pressure.

Threat of Substitutes — Moderate

Alternative candidate evaluation approaches including structured behavioral interviews, work sample tests, reference checks, and trial employment periods represent partial substitutes for psychometric testing. However, research consistently demonstrates that validated psychometric instruments achieve higher predictive validity than unstructured alternatives, mitigating substitution risk. AI-powered resume screening and social media analytics are emerging as complementary rather than substitute technologies in most deployments.

Competitive Rivalry — High

Competitive intensity in the psychometric tests market is high, driven by market fragmentation, technology commoditization at the lower end, and aggressive investment by technology-first challengers. Leading incumbents are defending market share through AI investment, platform expansion, and M&A. Price competition is intensifying in the SMB segment, while premium scientific rigor and integration depth remain key differentiators in the enterprise segment.

10. Strategic Recommendations

Based on the market analysis presented in this report, the following strategic recommendations are offered for stakeholders across the psychometric tests ecosystem:

For Assessment Vendors

- Invest in AI and adaptive testing capabilities to maintain competitive differentiation and meet candidate experience expectations. AI-adaptive modules that reduce test duration by 30–40% represent a compelling value proposition.

- Expand localization capabilities and culturally validated normative databases to capture growth in Asia-Pacific, Latin America, and MEA markets.

- Develop robust privacy-by-design architecture and pursue third-party ethical AI certification to meet evolving regulatory requirements under the EU AI Act and comparable frameworks.

- Build and deepen integrations with leading HCM platforms (Workday, SAP SuccessFactors, Oracle HCM) to embed assessments within existing talent workflows.

For Corporate HR Leaders

- Adopt a portfolio approach to psychometric testing, combining cognitive ability, personality, and situational judgment assessments to maximize predictive validity.

- Ensure all deployed assessments have documented adverse impact studies and that human oversight mechanisms are in place for AI-assisted screening decisions.

- Leverage longitudinal psychometric data within integrated talent management platforms to support succession planning and high-potential identification.

For Investors

- The psychometric tests market offers attractive risk-adjusted growth characteristics: high switching costs, recurring revenue models, and a structural tailwind from skills-based hiring trends.

- Focus investment on AI-native challenger platforms with strong scientific advisory boards and enterprise integration capabilities.

- Monitor regulatory developments around algorithmic hiring in the EU and US, which may create compliance-driven demand for tested and certified assessment vendors.