MARKET RESEARCH REPORT

Japan Stem Cells Market

Insights, Analysis & Forecasts to 2034

Published by GMI Reports | www.gmigreports.com

Executive Summary

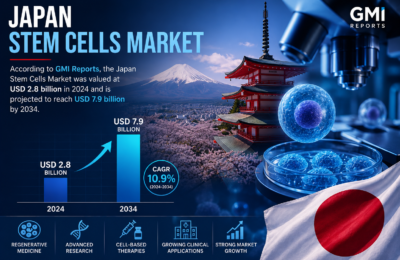

The Japan stem cells market represents one of the most scientifically advanced and commercially dynamic regenerative medicine ecosystems in the world. Valued at USD 2.8 billion in 2024, the market is projected to grow at a compound annual growth rate (CAGR) of approximately 11.0%, reaching USD 7.9 billion by 2034, according to GMI Reports. Japan’s unique regulatory environment, world-leading iPSC research infrastructure, and robust government investment in the life sciences collectively position it as a global frontrunner in translating stem cell science into clinical and commercial applications.

Japan holds a distinctive global position in the stem cell landscape due to the pioneering contributions of Nobel Prize laureate Professor Shinya Yamanaka, whose discovery of induced pluripotent stem cells (iPSCs) at Kyoto University in 2006 fundamentally transformed regenerative medicine worldwide. Building on this foundational breakthrough, Japan has constructed an unparalleled national iPSC research and banking infrastructure, most notably through the CiRA (Center for iPS Cell Research and Application) iPSC stock project.

The 2014 Act on the Safety of Regenerative Medicine and the revised Pharmaceutical and Medical Device (PMD) Act introduced expedited conditional approval pathways for regenerative medicine products, dramatically shortening time-to-market compared to conventional regulatory routes. This regulatory innovation has catalyzed a wave of clinical development activity and early commercial approvals that have further cemented Japan’s leadership position in the global stem cell market.

Market Overview

The Japan stem cells market encompasses the research, development, manufacturing, and clinical application of various categories of stem cells, including embryonic stem cells (ESCs), induced pluripotent stem cells (iPSCs), mesenchymal stem cells (MSCs), hematopoietic stem cells (HSCs), neural stem cells, and other specialized progenitor cell populations. Market participants include academic research institutions, biopharmaceutical companies, contract development and manufacturing organizations (CDMOs), hospital-based cell therapy programs, and dedicated stem cell product developers.

Japan’s research university network, anchored by institutions including Kyoto University, the University of Tokyo, Osaka University, and Keio University, constitutes the primary engine of scientific discovery in the stem cell field. These institutions maintain extensive collaboration networks with domestic and international industry partners, facilitating efficient translation of basic research insights into clinical development programs.

The commercial ecosystem encompasses a growing number of dedicated cell therapy companies alongside larger pharmaceutical and medical device corporations that have established regenerative medicine divisions. The Japan Agency for Medical Research and Development (AMED) serves as the principal public funding conduit for translational stem cell research, having disbursed billions of yen in competitive research grants since its establishment in 2015.

Market Size & Forecast

Market Driving Factors

1. World-Leading iPSC Research Infrastructure

Japan’s iPSC research ecosystem is unmatched globally in terms of institutional depth, public investment, and translational infrastructure. CiRA at Kyoto University maintains a clinical-grade iPSC bank covering a significant proportion of Japan’s HLA diversity, enabling the production of allogeneic iPSC-derived cell therapies with minimized immune rejection risk. This shared infrastructure substantially reduces the development costs and timelines for companies seeking to commercialize iPSC-based treatments, providing Japan’s cell therapy sector with a structural competitive advantage.

2. Expedited Regulatory Framework for Regenerative Medicine

Japan’s conditional and time-limited approval pathway under the PMD Act allows regenerative medicine products demonstrating probable efficacy and acceptable safety to receive market authorization ahead of completion of large-scale randomized controlled trials. Products must subsequently generate confirmatory evidence within a defined post-approval period. This pathway has enabled several pioneering approvals including the world’s first iPSC-derived cell therapy approval for age-related macular degeneration and cartilage repair applications, establishing proof-of-concept for the commercial viability of iPSC therapeutics.

3. Substantial Government Investment via AMED and National Programs

The Japanese government has committed substantial and sustained public funding to regenerative medicine research through AMED and broader life sciences strategy initiatives. The Strategic Center of Biomedical Advanced Vaccine Research and Development for Preparedness and Response (SCARDA) and related programs reflect Japan’s recognition of regenerative medicine as a strategic national technology priority. Government investment de-risks early-stage development and sustains a broad pipeline of stem cell research programs that feed into commercial development activity.

4. Aging Population and High-Prevalence Degenerative Disease Burden

Japan has the world’s most aged society, with over 29% of the population aged 65 or older in 2024. This demographic structure creates an exceptionally large and growing patient population for stem cell-based interventions targeting age-associated conditions including Parkinson’s disease, age-related macular degeneration, osteoarthritis, cardiac insufficiency, and neurodegenerative disorders. The overlap between Japan’s iPSC technological leadership and its domestic patient population represents a uniquely favorable market development dynamic.

5. National Health Insurance Coverage of Approved Cell Therapies

Several approved regenerative medicine products in Japan have secured National Health Insurance reimbursement coverage, substantially expanding patient access and market penetration. Reimbursement inclusion validates clinical value propositions for payers and providers, creating sustainable commercial revenue streams for product developers. The NHI coverage determination process for regenerative medicine products has become an important strategic milestone in commercial planning for Japanese and international cell therapy companies.

6. Expanding Industrial Manufacturing Ecosystem

Japan has invested heavily in developing industrial-scale cell therapy manufacturing capabilities. Multiple major pharmaceutical companies, specialized CDMOs, and public-private manufacturing consortia have established GMP-compliant cell processing facilities capable of producing allogeneic cell therapies at commercial scale. Process automation, closed bioreactor systems, and quality-by-design manufacturing approaches are being widely implemented to reduce batch-to-batch variability and enable cost-effective large-scale production.

Market Restraining Factors

1. High Development Costs and Long Development Timelines

Despite expedited regulatory pathways, stem cell therapy development in Japan remains a capital-intensive and time-consuming process. Clinical-grade cell manufacturing, quality control, clinical trial execution, and regulatory submission represent cumulative costs that are prohibitive for smaller organizations without substantial financial backing. Post-approval confirmatory trial requirements also impose ongoing commitments that maintain cost pressure through the commercial product lifecycle.

2. Reimbursement Uncertainty and Pricing Challenges

While some products have secured NHI coverage, reimbursement for novel and high-cost regenerative medicine products faces increasing scrutiny from Japan’s Central Social Insurance Medical Council (Chuikyo). The pricing methodology for cell therapies, which do not fit conventional pharmaceutical cost-effectiveness frameworks, remains in development. Reimbursement uncertainty creates commercial risk for product developers and can delay broad patient access following regulatory approval.

3. Technical Complexity in Scale-Up and Standardization

Transitioning stem cell manufacturing from laboratory to commercial scale introduces significant technical challenges in maintaining cell quality, potency, and consistency. Autologous cell therapy manufacturing faces inherent scalability constraints due to patient-specific production requirements. Even for allogeneic platforms, standardization of cell characterization, potency assays, and release criteria across production batches and facilities remains technically demanding and adds to regulatory burden.

4. Ethical and Social Considerations Around Embryonic Stem Cells

While iPSC research has largely superseded the ethical controversies associated with human embryonic stem cell (hESC) research, certain ESC-based research and development programs continue to navigate ethical oversight requirements and periodic public policy scrutiny. These considerations can create delays in research program approvals and may limit the scope of permissible scientific inquiry in specific cell biology domains.

Market Segmentation

By Cell Type

iPSCs command the largest and fastest-growing market share, reflecting Japan’s unique institutional and regulatory advantages in this technology category. The iPSC segment’s projected share expansion through 2034 mirrors the progressive maturation of iPSC-derived product pipelines toward clinical approval and commercial launch. MSCs retain a substantial market presence given their extensive clinical application history in immunomodulation, graft-versus-host disease, and orthopedic indications.

By Application

Drug discovery and toxicity testing represents the largest application segment by revenue, driven by widespread adoption of iPSC-derived cardiomyocytes, hepatocytes, and neurons as human-relevant in vitro models in pharmaceutical R&D. Regenerative medicine and cell therapy is the fastest-growing application segment and is projected to surpass drug discovery applications by the early 2030s as the clinical product pipeline matures.

By Product

By End-User

Competitive Landscape

The Japan stem cells market features a distinctive competitive structure comprising world-class academic institutions, specialized domestic biotech companies, major pharmaceutical corporations with regenerative medicine divisions, and a growing international company presence attracted by Japan’s regulatory and scientific environment. The market is moderately concentrated at the commercial product level, with a larger and more fragmented research tools and services segment.

Regulatory Landscape

Japan’s regulatory framework for stem cell and regenerative medicine products is administered primarily by the Pharmaceuticals and Medical Devices Agency (PMDA) under the overarching policy framework established by the Ministry of Health, Labour and Welfare (MHLW). The 2014 legislative reforms that introduced the Act on the Safety of Regenerative Medicine and the revised PMD Act created a dual-track system accommodating both conventional full approval and conditional/time-limited approval for regenerative medicine products.

The conditional approval pathway requires demonstration of probable efficacy based on limited clinical data, acceptable safety, and a commitment to conduct confirmatory post-approval trials within a specified timeframe (typically seven years). This pathway has enabled Japan to achieve a series of world-first regulatory milestones in iPSC-derived cell therapy, establishing it as the global benchmark for progressive regenerative medicine regulation.

PMDA has also established dedicated scientific consultation services for regenerative medicine product developers, providing early and iterative regulatory guidance to support clinical development planning. The agency has published comprehensive guidelines covering cell characterization, manufacturing quality, non-clinical safety assessment, and clinical trial design for stem cell products across multiple therapeutic categories.

Regional Analysis

Stem cell research and commercial activity in Japan is geographically concentrated in the major metropolitan research clusters, reflecting the distribution of Japan’s leading universities, teaching hospitals, and life sciences industrial zones.

Emerging Market Trends

Off-the-Shelf Allogeneic iPSC-Derived Cell Therapy

The most transformative commercial trend in Japan’s stem cell market is the progressive commercialization of off-the-shelf allogeneic iPSC-derived cell therapies enabled by the CiRA iPSC stock. Allogeneic products overcome the scalability and cost limitations of autologous approaches, enabling centralized manufacturing, quality-assured banking, and broad patient access. Multiple clinical programs targeting retinal disease, cardiac repair, neurological conditions, and hematological malignancies are advancing through the Japanese clinical pipeline using allogeneic iPSC-derived cell types.

Organoid Technology Integration

iPSC-derived organoid platforms are experiencing rapid adoption in Japanese pharmaceutical R&D as next-generation drug screening and disease modeling tools. Organoids derived from patient-specific iPSCs offer unprecedented human-relevant biological fidelity compared to conventional 2D cell culture systems. Major Japanese pharmaceutical companies including Takeda, Astellas, and Eisai have established organoid technology programs in partnership with academic institutions, creating a growing commercial demand for iPSC reagents, differentiation protocols, and organoid characterization services.

Cell Therapy Tourism and International Patient Access

Japan’s progressive regulatory framework and clinical availability of approved stem cell therapies has generated significant inbound medical tourism from patients in markets where comparable treatments are not yet approved. This dynamic creates additional revenue streams for Japanese hospitals and cell therapy centers with international patient service capabilities. Government and industry stakeholders are developing frameworks to manage international patient access in a manner that maintains patient safety standards while supporting the commercial sustainability of Japanese cell therapy providers.

Convergence with Gene Editing Technologies

The integration of CRISPR-Cas9 and other genome editing technologies with iPSC platforms is generating a new generation of engineered cell therapy candidates with enhanced efficacy and persistence profiles. Several Japanese academic groups and companies are developing gene-edited iPSC-derived immune cell therapies for oncology applications. This technological convergence is attracting substantial international partnership interest and is expanding the addressable market for Japan’s cell therapy sector.

Digital and AI Integration in Cell Manufacturing

Artificial intelligence and machine learning applications are being integrated into cell therapy manufacturing quality control, process optimization, and lot release decision-making in Japan. Computer vision systems for automated cell morphology assessment, predictive analytics for culture process control, and AI-assisted potency assay interpretation are reducing manufacturing variability and labor costs. Several Japanese CDMOs and instrument companies are commercializing AI-enabled cell manufacturing platform solutions targeting both domestic and international customers.

Key Companies in the Japan Stem Cells Market

-

Center for iPS Cell Research and Application (CiRA), Kyoto University

-

RIKEN BioResource Research Center

-

Healios K.K.

-

JCR Pharmaceuticals Co., Ltd.

-

Sumitomo Pharma Co., Ltd.

-

Takeda Pharmaceutical Company Limited

-

Rohto Pharmaceutical Co., Ltd.

-

Nipro Corporation

-

Astellas Pharma Inc. (Regenerative Medicine Division)

-

StemCyte Japan Inc.

-

Cynata Therapeutics (Japan Operations)

-

Terumo Corporation (Cell Therapy Division)

-

Fujifilm Cellular Dynamics International (FCDI Japan)

-

ReproCELL Incorporated

-

Other Academic Spinouts and Regional Biotech Companies

Report Target Audience

-

Biopharmaceutical and Cell Therapy Companies

-

Academic Research Institutions and Principal Investigators

-

Private Equity, Venture Capital, and Life Sciences Investors

-

Contract Development and Manufacturing Organizations (CDMOs)

-

Hospitals, Medical Centers, and Cell Therapy Clinics

-

MHLW, PMDA, and Government Health Policy Bodies

-

Stem Cell Banking Service Providers

-

Pharmaceutical Licensing and Business Development Teams

-

Management Consultants and Strategy Advisors in Life Sciences

Market Segmentation Summary

By Cell Type

-

Induced Pluripotent Stem Cells (iPSC)

-

Mesenchymal Stem Cells (MSC)

-

Hematopoietic Stem Cells (HSC)

-

Embryonic Stem Cells (ESC)

-

Neural Stem Cells

-

Other Stem Cell Types

By Application

-

Drug Discovery and Toxicity Testing

-

Regenerative Medicine and Cell Therapy

-

Stem Cell Banking

-

Research Reagents and Tools

-

Diagnostic Applications

By Product

-

Cell Therapy Products

-

Research Tools and Reagents

-

Stem Cell Banking Services

-

Contract Manufacturing Services

-

Instruments and Equipment

By End-User

-

Academic and Research Institutes

-

Biopharmaceutical Companies

-

Hospitals and Cell Therapy Centers

-

Contract Research Organizations

-

Stem Cell Banks

By Region

-

Kansai (Osaka-Kyoto-Kobe)

-

Kanto (Greater Tokyo)

-

Chubu (Nagoya area)

-

Kyushu

-

Tohoku and Other Regions

About GMI Reports

GMI Reports is a premier global market intelligence and research organization delivering data-driven insights and strategic analysis across a diverse range of industries. Our life sciences research practice provides in-depth coverage of biopharmaceutical, medical technology, and regenerative medicine markets across all major geographies. For the Japan Stem Cells Market report, related research, or bespoke intelligence solutions, visit www.gmigreports.com.

www.gmigreports.com