MARKET RESEARCH REPORT

Renewable Energy Market

Global Insights, Analysis & Forecasts to 2034

Published by GMI Reports | www.gmigreports.com

Executive Summary

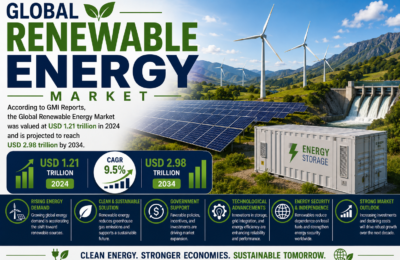

The global renewable energy market was valued at USD 1.21 trillion in 2024 and is projected to grow at a compound annual growth rate (CAGR) of approximately 9.5%, reaching USD 2.98 trillion by 2034, according to GMI Reports. The renewable energy sector has firmly established itself as the dominant driver of global new power generation capacity additions, with solar photovoltaic and wind technologies achieving cost parity or outright cost advantage relative to conventional fossil fuel generation across the substantial majority of global markets.

Continued technology cost declines, large-scale grid-connected battery storage deployment growth, and accelerating corporate renewable energy procurement have collectively sustained robust market expansion despite periodic policy uncertainty and supply chain volatility affecting specific national markets. China, the United States, and the European Union collectively continue to drive the substantial majority of global renewable energy capacity investment, while emerging markets across Asia, Latin America, and the Middle East increasingly represent significant incremental growth contributors.

The accelerating integration of renewable generation with grid-scale battery storage, green hydrogen production, and electric vehicle charging infrastructure is reshaping the renewable energy market’s commercial structure beyond pure electricity generation toward broader integrated energy system solutions. This systems-level integration trend is expected to define the next phase of renewable energy market evolution as grid operators and developers increasingly prioritize dispatchable and firm renewable energy capability.

Market Overview

The global renewable energy market encompasses electricity generation, associated equipment manufacturing, project development, and integration services spanning solar photovoltaic, onshore and offshore wind, hydropower, bioenergy, and geothermal energy technologies. The market serves utility-scale power generation, distributed and commercial/industrial generation, and increasingly residential-scale renewable energy adoption across virtually every global economy.

Solar photovoltaic technology has emerged as the dominant renewable energy capacity addition technology globally, driven by sustained manufacturing cost declines achieved through continuous technology improvement and substantial global manufacturing capacity expansion, particularly within China’s dominant photovoltaic manufacturing base. Wind energy, encompassing both established onshore wind technology and the rapidly maturing offshore wind sector, represents the second-largest renewable energy capacity contributor, with offshore wind technology increasingly unlocking substantial new project development potential in coastal regions with limited onshore wind resource availability.

The renewable energy market’s growth trajectory is increasingly shaped by its interdependent relationship with battery energy storage system deployment, which addresses the intermittency characteristics of solar and wind generation while enabling renewable energy’s expanding role in grid balancing and dispatchable power supply applications. This storage integration trend, combined with accelerating electrification of transportation and industrial heat applications, continues to expand the addressable market for renewable energy generation capacity globally.

Market Size & Forecast

Market Driving Factors

1. Sustained Technology Cost Decline and Grid Parity Achievement

Continued solar photovoltaic and wind technology cost declines, driven by manufacturing scale economics, technology efficiency improvements, and intensifying global supply chain competition, have established renewable energy as the lowest-cost new power generation source across the substantial majority of global markets. This fundamental cost advantage continues to drive renewable energy capacity investment even in markets with reduced direct policy support, reflecting renewable energy’s transition from a policy-dependent to an economically self-sustaining growth market.

2. Accelerating Corporate Renewable Energy Procurement

Major global corporations across technology, manufacturing, and retail sectors continue to substantially expand renewable energy procurement commitments through power purchase agreements and direct project investment, driven by corporate sustainability commitments, investor environmental, social, and governance expectations, and the compelling economic case for renewable energy as a long-term electricity cost hedge. Corporate procurement has become a significant and increasingly influential demand driver independent of government policy support mechanisms.

3. Battery Storage Integration Enabling Grid Dispatchability

The rapidly declining cost and expanding deployment scale of grid-connected battery energy storage systems is progressively addressing renewable energy’s historical intermittency limitations, enabling solar and wind generation to increasingly provide firm, dispatchable power supply capability. This storage integration trend is unlocking substantial additional renewable energy market growth potential by expanding the technology’s applicability beyond variable generation toward grid balancing and peak demand service provision.

4. Government Climate Policy and Net-Zero Commitment Implementation

Continued implementation of national and regional climate policy frameworks, including carbon pricing mechanisms, renewable portfolio standards, and economy-wide net-zero emissions commitments, sustains substantial policy-driven renewable energy demand across major global economies. While policy support intensity varies considerably across jurisdictions, the overall global policy trajectory continues to favor sustained renewable energy capacity expansion as a core climate mitigation strategy component.

5. Electrification of Transportation and Industrial Processes

Accelerating electric vehicle adoption and growing industrial process electrification, particularly within previously fossil fuel-dependent heating and manufacturing applications, is substantially expanding global electricity demand growth projections. This expanding electricity demand base creates significant incremental market opportunity for renewable energy capacity addition, as both policy frameworks and corporate sustainability commitments increasingly favor renewable sources for meeting this growing electrification-driven demand.

6. Energy Security and Diversification Priorities

Heightened global energy security concerns, intensified by geopolitical supply disruptions affecting conventional fossil fuel markets, have elevated renewable energy’s strategic value proposition as a domestically deployable energy source reducing import dependency. This energy security dimension has broadened renewable energy’s political and economic support base beyond climate policy considerations alone, sustaining investment momentum even amid periods of broader climate policy debate or uncertainty.

Market Restraining Factors

1. Grid Infrastructure and Transmission Capacity Constraints

Many major global markets face substantial grid transmission infrastructure constraints limiting the pace at which new renewable energy capacity can be interconnected and effectively utilized. Lengthy grid interconnection queues, transmission infrastructure development timelines often extending considerably longer than renewable project construction periods, and curtailment of generated renewable electricity due to insufficient transmission capacity collectively constrain the realized market growth potential relative to underlying project development pipeline scale.

2. Supply Chain Concentration and Trade Policy Volatility

The renewable energy manufacturing supply chain, particularly within solar photovoltaic component manufacturing, exhibits substantial geographic concentration that creates both supply chain resilience concerns and trade policy volatility risk for project developers across different national markets. Tariff implementation, trade dispute resolution uncertainty, and periodic supply chain disruption affecting key component availability continue to introduce cost and timeline unpredictability into renewable energy project development.

3. Land Use, Permitting, and Community Acceptance Challenges

Large-scale renewable energy project development, particularly for utility-scale solar and onshore wind installations, continues to encounter land use competition, environmental permitting complexity, and local community acceptance challenges that can substantially extend project development timelines or constrain project siting flexibility. These development friction factors vary considerably across jurisdictions but represent a persistent market growth constraint requiring continued industry and policy engagement to address.

4. Raw Material and Critical Mineral Supply Constraints

Renewable energy technology manufacturing, particularly for wind turbine permanent magnets and battery storage systems, depends substantially on critical mineral inputs facing their own supply concentration and extraction capacity expansion constraints. These critical mineral supply considerations introduce potential cost and availability risk factors that could moderate renewable energy technology cost decline trajectories or constrain manufacturing capacity expansion pace under certain supply scenario assumptions.

Market Segmentation

By Energy Source

Solar photovoltaic technology maintains the leading and fastest-growing market share position, driven by its sustained manufacturing cost decline trajectory and applicability across utility-scale, commercial, and residential deployment scales. Wind energy retains substantial and stable market share, with offshore wind technology increasingly contributing an expanding proportion of overall wind sector capacity growth as the technology matures and project economics continue to improve.

By Application

Utility-scale power generation applications retain the dominant market revenue share, reflecting the substantial capital scale and grid integration focus of major renewable energy project development globally. The commercial and industrial segment continues to exhibit strong growth, driven by accelerating corporate renewable energy procurement and on-site generation investment trends across major global corporations.

By End-Use

Competitive Landscape

The global renewable energy market features a combination of major diversified utility and independent power producer companies with extensive renewable project development and ownership portfolios, alongside specialized equipment manufacturers spanning solar module, wind turbine, and battery storage technology categories. Market competition increasingly centers on project development pipeline scale, technology cost leadership, and integrated energy system solution capability.

Regional Analysis

Asia Pacific represents the largest global renewable energy market, anchored by China’s dominant manufacturing base and substantial domestic capacity deployment, alongside significant contribution from India and Southeast Asian markets. North America and Europe represent substantial established markets with mature policy frameworks, while the Middle East and Latin America are increasingly significant emerging growth markets.

Emerging Market Trends

Co-located Renewable and Battery Storage Project Development

Project developers are increasingly designing renewable energy installations with co-located battery storage systems from initial project conception, rather than retrofitting storage capability to existing generation assets. This integrated design approach optimizes grid interconnection efficiency, enhances project revenue stability through energy arbitrage and grid service provision capability, and increasingly represents the standard development approach for new utility-scale renewable energy projects.

Green Hydrogen Production Integration

Growing renewable energy project development increasingly incorporates green hydrogen production capability, utilizing renewable electricity for water electrolysis to produce hydrogen for industrial, transportation, and energy storage applications. This integration trend reflects renewable energy’s expanding role beyond direct electricity supply toward broader energy carrier and industrial feedstock production applications, particularly within heavy industry decarbonization strategies.

Floating Solar and Offshore Wind Technology Expansion

Continued technology advancement in floating solar photovoltaic systems and floating offshore wind platforms is unlocking substantial new renewable energy development potential in water-based locations previously unsuitable for conventional ground-mounted or fixed-bottom installations. These floating technology categories represent significant emerging growth opportunities, particularly within land-constrained markets and deep-water coastal regions with strong offshore wind resource potential.

AI-Driven Grid Management and Renewable Forecasting

Advanced artificial intelligence and machine learning applications are increasingly deployed for renewable energy generation forecasting, grid balancing optimization, and predictive maintenance across both project-level and grid-system-level operations. These AI-driven capabilities are improving renewable energy integration efficiency and reducing the operational complexity historically associated with managing variable generation resources at scale.

Repowering and Asset Lifecycle Extension

A growing share of renewable energy market activity involves repowering of aging wind and solar installations with upgraded, higher-efficiency technology, extending project lifecycles and substantially increasing energy output from existing development sites. This repowering trend represents an increasingly significant market activity category as the renewable energy sector’s installed base matures, particularly within early-adopter markets with substantial first-generation renewable capacity approaching technology refresh cycles.

Key Companies in the Renewable Energy Market

-

NextEra Energy

-

Iberdrola S.A.

-

Ørsted A/S

-

China Three Gorges Corporation

-

EDP Renováveis

-

Vestas Wind Systems

-

First Solar Inc.

-

LONGi Green Energy

-

Siemens Gamesa

-

Enel Green Power

-

Other Regional and Independent Power Producers

Report Target Audience

-

Renewable Energy Developers and Independent Power Producers

-

Equipment Manufacturers (Solar, Wind, Storage)

-

Electric Utilities and Grid Operators

-

Investment and Private Equity Firms

-

Government Energy and Climate Policy Agencies

-

Corporate Sustainability and Energy Procurement Teams

-

Management and Strategy Consultants

-

Academic and Energy Policy Research Institutions

Market Segmentation Summary

By Energy Source

-

Solar Photovoltaic

-

Wind (Onshore & Offshore)

-

Hydropower

-

Bioenergy

-

Geothermal & Other

By Application

-

Utility-Scale Power Generation

-

Commercial & Industrial

-

Residential

By End-Use

-

Electric Utilities

-

Industrial & Manufacturing

-

Commercial Buildings

-

Residential

By Region

-

Asia Pacific

-

North America

-

Europe

-

Latin America

-

Middle East & Africa

About GMI Reports

GMI Reports is a premier market intelligence and research organization providing data-driven insights and strategic analysis across global energy, utilities, and infrastructure markets. Our research empowers developers, utilities, and investors to navigate the evolving renewable energy landscape with confidence. For the Renewable Energy Market report and related research, visit www.gmigreports.com or contact our research team for customized intelligence solutions.

www.gmigreports.com