France Battery Energy Storage System Market

Insights & Forecasts to 2035

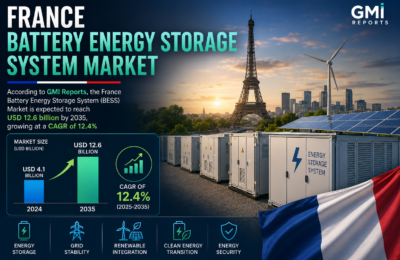

According to a research report published by GMI Reports, the France Battery Energy Storage System (BESS) Market Size is anticipated to reach USD 12.6 Billion by 2035, growing at a CAGR of approximately 12.4% from 2025 to 2035. France’s ambitious energy transition agenda, rapid deployment of renewable energy infrastructure, and strong governmental policy support are the primary catalysts driving market expansion across the forecast period.

Market Overview

The France Battery Energy Storage System (BESS) market encompasses technologies and solutions designed to store electrical energy generated from renewable and conventional sources for subsequent use. These systems serve as critical enablers of grid stability, peak shaving, frequency regulation, and energy arbitrage across utility, commercial, industrial, and residential applications. France’s commitment under the European Green Deal and its national low-carbon strategy has accelerated the integration of lithium-ion, flow battery, and solid-state storage technologies throughout the country.

Key factors stimulating market momentum include:

-

Rapid expansion of solar and wind power capacity requiring grid-scale buffer storage

-

Government incentives and European Union-backed subsidies for clean energy infrastructure

-

Growing adoption of distributed energy resources (DERs) among French households and enterprises

-

Advancements in battery chemistries reducing cost per kWh and extending operational lifespans

-

Rising electricity price volatility encouraging businesses to invest in self-consumption storage

-

Digital grid modernization integrating smart energy management systems with BESS platforms

Report Coverage

This research report provides a comprehensive analysis of the France Battery Energy Storage System market, segmented by technology, application, connection type, and end user. The study covers historical data from 2020 through 2024 and provides detailed revenue forecasts extending to 2035. The report evaluates competitive dynamics, regulatory influences, investment trends, and supply chain developments. Recent strategic activities including capacity expansions, technology partnerships, mergers and acquisitions, and project announcements have been incorporated to reflect the evolving competitive landscape.

Driving Factors

France’s accelerating renewable energy capacity additions are a principal driver of BESS demand. The government’s Multi-Year Energy Plan (PPE) mandates significant reductions in carbon emissions and increased shares of solar, wind, and hydropower in the national energy mix, creating robust storage requirements at both grid and distributed levels. European Union directives on energy storage and flexibility markets further provide regulatory clarity, encouraging long-term project investment.

Declining battery pack costs—particularly for lithium-iron-phosphate (LFP) chemistries—are broadening the accessible market across residential rooftop, commercial and industrial (C&I), and utility-scale segments. Additionally, rising consumer awareness of energy independence, coupled with net metering policies and time-of-use tariff structures, is motivating household-level BESS adoption. Electrification of transport is also generating demand for vehicle-to-grid (V2G) integration, positioning BESS as a multifunctional asset class.

Restraining Factors

Despite strong growth fundamentals, several headwinds could temper market expansion. High upfront capital costs for utility-scale BESS installations remain a barrier for smaller project developers lacking access to green financing. Supply chain dependencies on critical battery minerals—including lithium, cobalt, and nickel—expose the market to commodity price volatility and geopolitical sourcing risks. Permitting complexity and lengthy grid connection approval timelines in France can also delay project commissioning, increasing development costs. Furthermore, limited standardization of second-life battery repurposing and end-of-life recycling infrastructure presents sustainability challenges as the installed base scales.

Market Segmentation

The France Battery Energy Storage System market is classified by technology, application, connection type, and end user.

By Technology

The lithium-ion segment commanded the largest market share in 2024 and is projected to sustain its leadership throughout the forecast period. Its dominance is underpinned by mature manufacturing ecosystems, favorable energy density-to-cost ratios, and broad applicability across utility, commercial, and residential deployments. Flow battery technologies, including vanadium redox and zinc-bromine variants, are gaining traction for long-duration storage applications where cycle longevity and depth of discharge are prioritized. Emerging solid-state battery chemistries are expected to enter commercial deployment phases post-2028, potentially reshaping segment dynamics.

By Application

Grid-scale energy storage represents the largest application segment, driven by transmission system operators’ requirements for frequency regulation, voltage support, and ancillary services procurement. Behind-the-meter storage for commercial and industrial users constitutes the fastest-growing application segment, fueled by corporate sustainability mandates and rising industrial electricity costs. Residential storage is also expanding, particularly in regions with high solar self-consumption rates and favorable prosumer tariff frameworks.

By Connection Type

On-grid connected BESS installations dominate the French market, reflecting the scale of utility and commercial projects integrated with the national transmission and distribution grid. Off-grid storage systems serve niche remote and island applications, including overseas French territories, where grid extension is economically unfeasible.

By End User

Utilities and grid operators represent the leading end-user segment, procuring large-scale BESS for ancillary services, renewable integration, and infrastructure deferral. Commercial and industrial users form the second-largest segment, leveraging storage for demand charge management and backup power. The residential end-user segment, while smaller in absolute capacity terms, is the fastest growing, with rooftop solar-coupled storage systems gaining market penetration across French urban and peri-urban regions.

Competitive Analysis

The France Battery Energy Storage System market features a combination of global technology leaders, European energy utilities, and specialized domestic integrators. Competition is characterized by technology differentiation, financing capabilities, project development expertise, and service offerings across the storage value chain. Key strategic activities include technology licensing agreements, joint ventures with French energy companies, and investment in local manufacturing to comply with European content requirements under emerging battery regulations.

Key Target Audience

-

Market Players and Technology Vendors

-

Energy Utility Operators and Grid Operators

-

Investors and Private Equity Firms

-

Government Authorities and Regulatory Bodies

-

Consulting and Research Firms

-

Venture Capitalists and Green Finance Institutions

-

Value-Added Resellers (VARs) and System Integrators

Market Segment Summary

This study forecasts revenue at France national and regional levels from 2020 to 2035. GMI Reports has segmented the France Battery Energy Storage System market based on the below-mentioned categories: